Hi there! Welcome to European Aluminium’s newsletter, your go-to source for policy insights shaping the future of Europe’s aluminium sector. In each edition, we highlight key industry developments and explore our top policy priorities to ensure a competitive, low-carbon aluminium sector that drives Europe’s green transition and strengthens its strategic autonomy.

From Ambition to Action 🔎

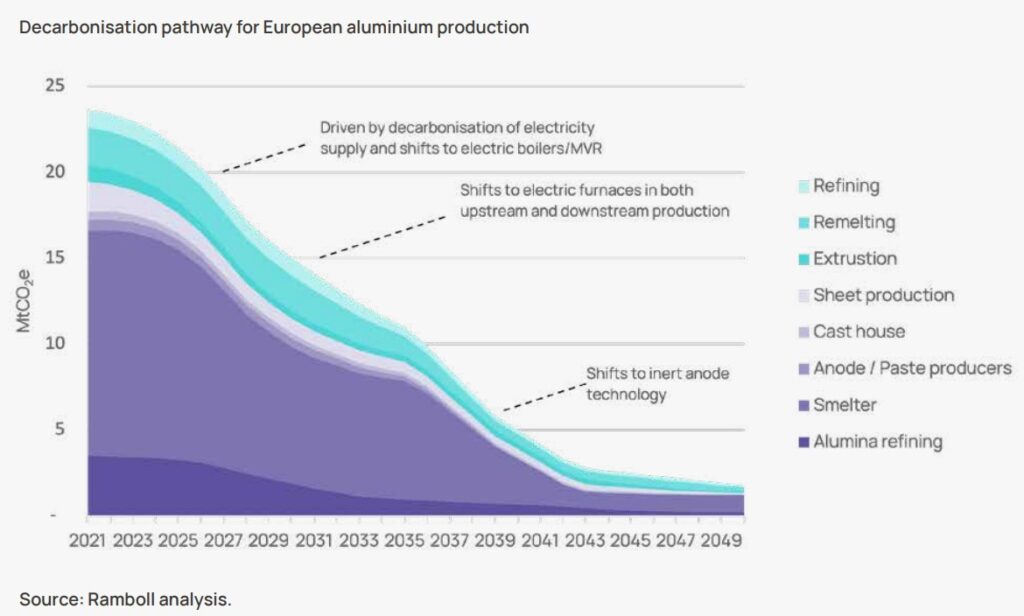

Aluminium is a strategic material for Europe’s green transition, enabling the deployment of essential clean technologies such as solar panels, wind turbines, electric vehicles and more. At the same time, it remains a hard-to-abate industrial sector, particularly due to its energy intensity, making our decarbonisation journey all the more urgent. To align with the IPCC’s 1.5°C scenario by 2050, the European aluminium industry must reduce its greenhouse gas emissions by 93%— from around 24 MtCO₂e today (mostly linked to primary production) to less than 2 MtCO₂e.

It’s an ambitious goal, but one that is within reach.

Decarbonising the European aluminium industry by 2050 is a shared commitment—and one that demands more than ambition: it calls for decisive, coordinated action. Our industry fully supports the EU’s climate objectives, but key barriers on the path to deep decarbonisation must be addressed.

🎥 In this month’s video, Sandro Starita , our Director of Sustainability, outlines the main challenges ahead and the steps needed to achieve full decarbonisation by 2050. Watch below 👇

Policy Action and Barriers: What’s Needed to Deliver a Decarbonised Aluminium Industry 🏛️⚡

The journey to decarbonisation demands the rapid advancement and deployment of innovative technologies for both process and combustion emissions. While research in these areas is advancing, they still require scaling, further development and targeted support.

Industry cannot achieve this transformation alone. Collaboration with stakeholders is essential, and key enablers are expected from the EU institutions:

✔️ Prioritise and boost investments in R&D and pilot deployment of low-carbon technologies through R&D grants, streamlined innovation funding, and stronger coordination with industrial needs. For example, inert anode technology—a breakthrough technology that can eliminate direct emissions from primary aluminium production—needs additional funding to become commercially viable. In the meantime, Carbon Capture and Storage (CCS) can play a bridging role, if made cost-effective through public support.

✔️ Ensure the availability to clean, affordable and secure electricity and other energy carriers (e.g. hydrogen). For primary aluminium production— a highly electro-intensive process—indirect emissions represent a significant share of the sector’s carbon footprint. Therefore, the EU must accelerate the decarbonisation of the power grid and improve the availability of competitively priced renewable electricity. Expanding access to Power Purchase Agreements (PPAs) and supporting self-generation of clean power will be vital to ensuring the transition without losing competitiveness.

✔️ Maximise aluminium scrap recovery and high-quality recycling. Recycling uses just 5% of the energy needed for primary aluminium production and is already a European strength—but there’s still room to grow. EU policies should support increased collection, investments in advanced sorting technologies, and incentives to boost recycling performance. Most importantly, stopping scrap leakage, which limits the availability of high-quality secondary material, is critical to closing the loop and reducing emissions.

✔️ Avoid poorly designed policy instruments. A good example is the EU Carbon Border Adjustment Mechanism (CBAM): a study commissioned by European Aluminium makes it clear that CBAM is not fit for purpose for our sector and will actually lead to increased carbon leakage, thus weakening Europe’s climate goals and reducing available resources for investing in decarbonisation and R&D. We urge EU policymakers to urgently “stop the clock” on CBAM implementation for aluminium until these critical flaws are resolved.

Last but certainly not least, the EU must incentivise and support low-carbon and circular aluminium production in Europe. Boosting domestic capacity—both secondary and primary—is not only vital for supply security, but also a climate imperative. European primary aluminium’s carbon footprint is less than half of the global average and around 40% lower than the imported material. Supporting its survival and growth is essential to reaching climate goals while maintaining a resilient, competitive European industry.

Financing the Future: Unlocking EU Funds to Support Aluminium Decarbonisation 💶

Deploying decarbonisation technologies for aluminium in Europe will entail a significant financial effort of over €30 billion, a figure that does not account for the essential research and development needed to innovate and scale the solutions. The industry cannot shoulder these investments alone, especially while struggling to remain competitive on a global playing field that is uneven, distorted by non-market forces, and marked by much higher energy prices than those faced by international competitors.

To develop and scale clean technologies, existing EU support mechanisms must be adapted to better reflect the needs of energy-intensive industries, like ours:

- At least 50% of ETS revenues must be reinvested in energy-intensive sectors to support their transition. This would also increase transparency on how Member States use these funds. Additionally, the ETS Innovation Fund should ensure fairer access and more impactful use of EU climate finance by simplifying and streamlining its functioning, especially for smaller companies.

- The recently announced draft European Competitiveness Fund should, once in force, make funding more accessible and support a continent-wide industrial revival, helping close the competitiveness gap with global players such as the U.S. and China. This fund, through its strategic pillar “Clean Transition and Industrial Decarbonisation”, could be a game-changer —if it delivers on its promise of being more predictable, streamlined, and private-sector friendly.

- The expected opening of Horizon Europe funding in 2026-27 to collaborative projects up to TRL 8 (the level of industrial demonstrators) should help the deployment of decarbonised technology solutions for energy-intensive industries in Europe and facilitate crossing the valley of death between innovation and industrial implementation.

- We also welcome the planned Industrial Decarbonisation Bank (IDB), expected in Q2 2026, which aims to mobilise up to €100 billion to accelerate the decarbonisation of Europe’s energy-intensive sectors. We strongly hope it will take into account the challenges of the aluminium industry—including support not only for breakthrough or one-of-a-kind technologies, but also for wide-scale deployment of mature solutions across all production processes.

Ensuring that the aluminium industry’s journey to decarbonise is fully supported by EU funding is essential—not only to meet our climate targets, but to secure the future of a resilient, innovative, and strategic European industry.

GET INVOLVED: JOIN THE CONVERSATION

Jump into the conversation and drop your thoughts on our Aluminium Action Plan and policy goals. Your insights and feedback are needed as we work towards a stronger, more resilient aluminium industry in Europe. Connect with us on LinkedIn and our website and stay updated on the latest developments!